Well folks, it's been a fun 10-year run at this little website. I'm moving on to a new platform: Substack!

Here's the new Noahpinion:

https://noahpinion.substack.com/

Thanks for reading, and hope to see you at the new site!

Here's the new Noahpinion:

https://noahpinion.substack.com/

Thanks for reading, and hope to see you at the new site!

It is not obvious that Japan “has lots of poverty.”...Smith here relies on a useless measure of “relative” poverty, the share of the population earning less than half of the median income. You can see the limitations of that approach: A uniformly poor society in which 99 percent of the people live on 50 cents a day and 1 percent live on 49 cents a day would have a poverty rate of 0.00; a rich society with incomes that are rising across-the-board but are rising much more quickly for the top two-thirds would have a rising poverty rate, and some people who are not classified as being in poverty this year might be in poverty next year even though their incomes are higher, etc. It would be far better to consider poverty in absolute terms, but our progressive friends are strangely resistant to that.Let's leave aside the question of whether poverty is best conceived of in absolute or relative terms. There are good arguments on both sides (and perhaps room for even more definitions of poverty than those two!). But it's definitely true that the average Japanese poor person enjoys a significantly higher standard of living than the average poor person in, say, Ethiopia.

Secondly, it is not entirely clear that the Japanese are as free from the pathologies that attend poverty in many other places as Smith suggests. It is true that Japan as a whole has low rates of chronic unemployment, drug use, single motherhood, etc., but the relevant question here would be how Japanese who are poor compare on these metrics with Japanese at large. To assume that the situation with the poor can be approximately deduced from national averages is pretty sloppy analysis, if it counts as analysis at all.Williamson is wrong about the relevant question. The relevant question is P(relative poverty | absolute bad behavior). In other words, the relevant question is: "How much does bad behavior change my chances of falling into the lower echelons of my developed country?". The percentage of Japanese people who are badly behaved is much smaller than the percentage of Americans who are badly behaved. Yet about the same fraction of people there fall into the lower echelons of that society (which, as noted above, are actually lower in absolute terms than the lower echelons of American society, at least at the 25th percentile). Thus, even if there are individual Japanese people who become poor due to bad behavior, it can't statistically be the biggest factor, as long as poverty has roughly the same causes in both countries.

Third, it emphatically is not the case that Japan is a society that is largely free from substance abuse. In Japan, as in the United States, the most socially significant and destructive mode of substance abuse is legal: alcohol abuse. Japan has a big problem with alcohol, and alcohol abuse is related to joblessness and poverty, although the question of causality (Are they unemployed because they drink, or do they drink because they are unemployed?) gets complicated, and some studies suggest that in Japan some kinds of destructive drinking increase with income.It's true that alcohol is typically the drug of choice in Japan. But even here, America is worse-behaved. Several different data sources all agree that the number of alcoholic drinks consumed per person in Japan is around 7, while the number in America is around 9. France, Germany and Australia, which have lower poverty rates than the U.S., are around 12.

Smith is correct that Japan has high work-force participation, and that it has a universal(ish) national health-insurance scheme. To which he adds: “Too many people fall through the cracks in the capitalist system because of unemployment, sickness, injury or other forms of bad luck.” This is an odd thing to write immediately after noting that Japan has 1. low unemployment and 2. a national health-care system that helps people through sickness and injury.

Perhaps those things are not sufficient?This is absolutely true; these things are not sufficient. But nowhere did I say they are.

“Capitalism” is a very broad term. The United States is a capitalist country, and a rich capitalist country at that. So is Japan. So is Singapore. So is Sweden. So is Switzerland. These countries have radically different health-care systems, tax codes, family lives, cultural norms, etc. Unsurprisingly, these produce different outcomes on a great many social fronts — but all of them are comprehended by “capitalism.”...To argue that the problem is “the capitalist system” is to retreat into generality and to refuse to consider the facts of the case, each on its own merits.It is true that different advanced countries have different systems, and that labeling them "capitalism" tends to obscure more than it clarifies. In fact, I recently wrote a whole article about that topic, which Williamson should read!

In New York, Los Angeles, and other big cities, it is common for people to sleep on the streets even as beds in shelters go unoccupied. There are many reasons for that, but the main one almost certainly is mental illness (and substance abuse as a subset of that). That is the nearly universal opinion of the professionals who work with the urban homeless.

There are better and worse ways to deal with mental illness in a wealthy, complex society, and we in the United States have settled on one of the worst: After the “deinstitutionalization” of the 1960s and 1970s, in which left-wing liberationist thinking combined with right-wing penny-pinching to gut the public mental hospitals, we punted the problem to the police and to the jailers, who are ill-equipped to handle it. The United States is not alone in this. Many (perhaps most) Western European countries have more effective social-welfare systems than we do, but even in Sweden, with its fairly comprehensive welfare state, mental illness is the leading cause of “work force exclusion,” as they call it.

[T]he big changes that progressives generally propose for the United States — a national health-care system like Japan’s, an enlarged welfare state more like Sweden’s — do not seem to have been entirely effective in the places where they have been tried. And there is good reason to believe that Swedish or Swiss practice cannot simply be imported into Eastern Kentucky or Baltimore and replicated locally. That does not mean that there is nothing to learn from Japanese or European practice — perfection is not our criterion — but it does complicate the conversation. We have, in fact, spent a tremendous amount of money on anti-poverty and economic-development programs, and much of that has not delivered anything like the promised return.

In my own reporting on poverty in the United States, I have tried to present the facts as unsparingly as I can. Perhaps Noah Smith thinks that I do this in order to savor the exquisite delights of moral condemnation. But the intended purpose is to scour away the crust of sentimentality that poverty has acquired in order that we may deal with the actual facts of the case in a way that is productive and that does not end up deepening the very problems we hope to mitigate. (emphasis mine)

Yes, young men of Garbutt — get off your asses and go find a job...

[N]obody did this to them. They failed themselves...There wasn’t some awful disaster. There wasn’t a war or a famine or a plague or a foreign occupation. Even the economic changes of the past few decades do very little to explain the dysfunction and negligence — and the incomprehensible malice — of poor white America...

The truth about these dysfunctional, downscale communities is that they deserve to die. Economically, they are negative assets. Morally, they are indefensible. Forget all your cheap theatrical Bruce Springsteen crap. Forget your sanctimony about struggling Rust Belt factory towns and your conspiracy theories about the wily Orientals stealing our jobs. Forget your goddamned gypsum, and, if he has a problem with that, forget Ed Burke, too. The white American underclass is in thrall to a vicious, selfish culture whose main products are misery and used heroin needles.And in the article Williamson himself cites, he wrote:

Thinking about the future here and its bleak prospects is not much fun at all, so instead of too much black-minded introspection you have the pills and the dope, the morning beers, the endless scratch-off lotto cards, healing meetings up on the hill, the federally funded ritual of trading cases of food-stamp Pepsi for packs of Kentucky’s Best cigarettes and good old hard currency, tall piles of gas-station nachos, the occasional blast of meth, Narcotics Anonymous meetings, petty crime, the draw, the recreational making and surgical unmaking of teenaged mothers, and death...If this represents "scouring away the crust of sentimentality", what does poverty reporting look like with the crust of sentimentality still on??

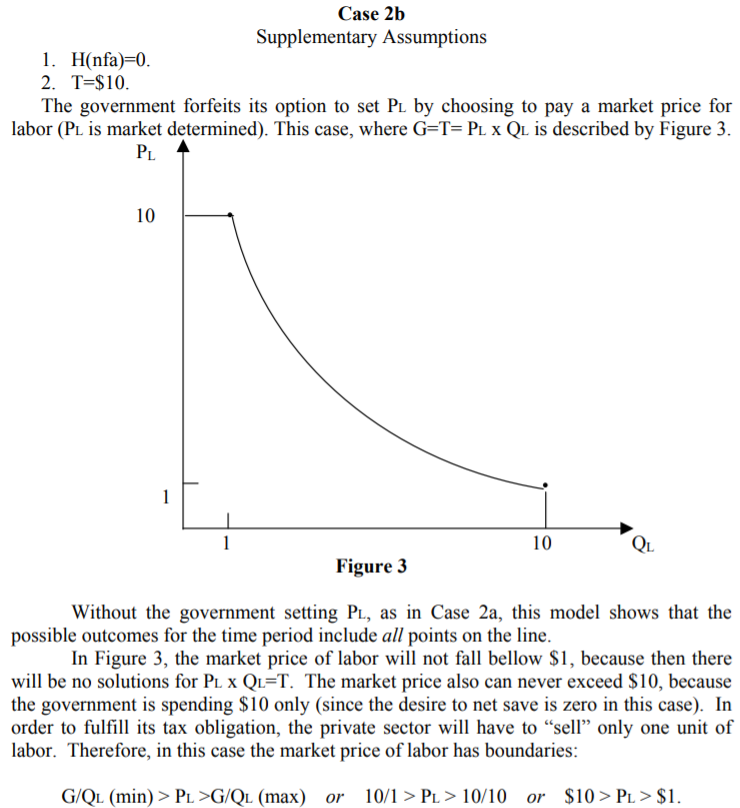

The critical economic policy question is what does the power to money finance deficit spending mean for government’s ability to promote full employment with price stability? This question can only be answered by placing that power within a theoretical model and exploring its implications...Proponents of MMT have a professional obligation to provide [a simple mathematical] model to help understand and assess the logic and originality of their claims. Yet, [MMT proponents Eric Tymoigne and L. Randall Wray] again fail to produce a model...If MMT-ers did produce a model, I am convinced the issues would become transparent, but readers would also see there is “no there there”.Now, a lot of people like to criticize mathematical models in economics. And they do have their drawbacks. Economists can sometimes become so entranced by the precision of math that they ignore the need to connect that math with the real world. And the difficulty of hacking through math can lead economists to make the models too simple.

"Functional finance" is a doctrine originated and set out by Abba Lerner...When I said that "functional finance" is at the core of MMT, I got immediately smacked down by one of the gurus...Perhaps the key to the eagerness of [L. Randall] Wray to dismiss me (and James Montier) for saying that MMT is Lerner+ is sociological. Perhaps MMT is not model-based ("IS-LM with a near-vertical IS curve") and not idea-based ("Functional Finance") so that it can be guru-based. (emphasis mine)It wasn't just DeLong and Montier who conflated MMT with Functional Finance. Aryun Jayadev and J.W. Mason did something similar in their attempted write-up of MMT, leading Josh Barro to do the same thing in his own criticism of MMT. Mason, Jayadev, and Barro criticized MMT on the grounds that raising taxes to control inflation - something you have to do in Functional Finance, and which some MMT advocates agree is necessary - is politically very difficult.

Yes, MMT does have another tool to maintain price stability. It is the JG approach to full employment. It has always been a core element of MMT. We have never relied the simplistic version of Functional Finance that was presented by Mason. It would take about five minutes of actual research to demonstrate this.Now that's a perfectly fine rebuttal. People get theories wrong all the time. It's perfectly possible that Mason, Jayadev, Barro, Montier, and DeLong were all very wrong to conflate MMT with Functional Finance, and that five minutes of actual research would have demonstrated this.